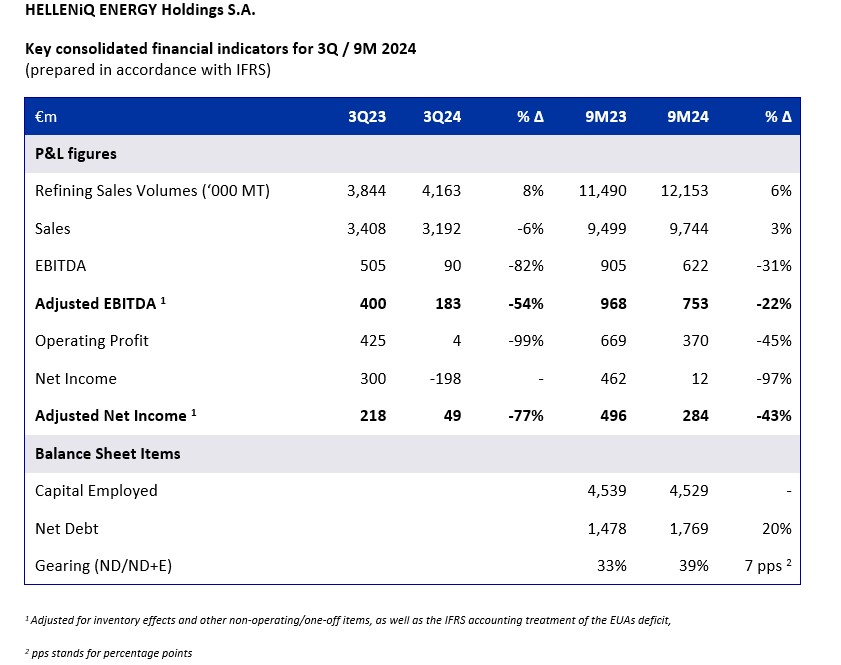

HELLENiQ ENERGY Holdings S.A. ("Company") announced its 3Q24 consolidated financial results, with Adjusted EBITDA amounting to €183m and Adjusted Net Income to €49m, while for 9M24 they amounted to €753m and €284m respectively.

Performance has been positively affected by increased refining units availability, leading to higher sales and improved operations, partly offsetting weaker refining margins, while Marketing and Petrochemicals’ performance also improved in 3Q24.

Downstream output in 3Q24 increased by 6% to 3.9m MT, while sales reached 4.2m MT (+8%), at the highest level since 3Q16, with exports corresponding to 46% of the total.

On 19 July 2024, L.5122 was passed for the imposition of a temporary Solidarity Contribution, which is calculated on the tax profits of FY23, which exceed 120% of the average respective results of 2018-2021, in accordance with the relevant European Regulation. The extraordinary contribution, on top of normal corporate taxation, amounts to €223m and will be paid in February 2025. The net impact on 3Q24 Reported Net Income amounts to €173m.

Considering the 9M24 results and the outlook for the FY24 period, the Board of Directors of HELLENiQ ENERGY Holdings decided the distribution of an interim dividend of €0.20 per share to its shareholders.

Main developments - Strategy implementation

The Group’s strategic plan’s implementation continues through initiatives targeting operational excellence and profitability improvement across all Group’s businesses, as well as the evaluation of options in relation to our participations in ELPEDISON and DEPA Commercial, aiming at increasing the Group’s value.

In Refining and Petrochemicals, energy autonomy and efficiency projects are progressing, while works relating to the expansion of the polypropylene plant’s capacity by 60,000 tons p.a. have commenced and are expected to be completed in the next two years. At the same time, initiatives focused on decarbonizing operations and improving the environmental footprint are advancing. As the majority of sales are carried out outside of the Greek market, the Company proceeded to transform the business model of its Supply & Trading business, through strengthening the team, implementing advanced systems and establishing trading subsidiaries in international markets.

In Marketing, the ongoing transformation program emphasizes on the rationalization and development of the retail network both in Greece and internationally, with a particular focus on strengthening our own network and promoting the sale of premium products, while also increasing the contribution from non-fuel sales of products and services. At the same time, emphasis is also placed on the expansion of the loyalty program.

In the Renewable Energy sources (RES) business, HELLENiQ RENEWABLES operates and develops projects totaling 5.7 GW in Greece and internationally. Specifically, projects with an installed capacity of 0.4 GW are already operational, while an additional 0.7 GW are under development and expected to be completed in the short term, with 120 MW expected to be added by the end of the year; with 0.5 GW of projects in operation, annual power generation is projected to reach 1 TWh, exceeding the annual electricity consumption of downstream business. The objective is to operate at least 1 GW of RES projects until 2026 and to exceed 2 GW by 2030.

In E&P business, seismic surveys have been completed in five offshore areas and data processing and interpretation is progressing, with a decision on drilling potential targets anticipated within 2025.

The implementation of the digital transformation program across all activities within the Group is ongoing, with substantial benefits projected for 2024, estimated at approximately €40m annually. Emphasis is placed on enhancing operational performance, ensuring the safety of personnel and facilities with a strong focus on preventive measures, and achieving more effective risk management.

Lower crude oil prices and benchmark refining margins

In 3Q24, Brent crude oil declined to the lowest levels since December 2021, averaging $80/bbl, a 7% decrease compared to 3Q23. The EUR/USD exchange rate averaged 1.10 vs 1.09 in 3Q23.

In contrast, natural gas and electricity prices increased by 5% and 17% respectively. At the same time, CO2 prices (EUAs) fell by 20% on average, compared to last year.

Refining margins dropped vs both 3Q23 and 2Q24. Specifically, our refineries’ system benchmark margin averaged $3.6/bbl in 3Q24 vs $12.6/bbl in 3Q23.

During 4Q24 (from October to 14 November 2024), refining margins have recovered slightly, with the system benchmark refining margin at approximately $5.5/bbl, albeit lower than the corresponding period of the previous year.

Increased demand for fuels in the domestic market

Domestic market demand in 3Q24 reached 1.7m MT, 2% higher than 3Q23, with automotive fuels consumption increasing by 3%. Aviation and marine fuels demand grew by 10% and 6% y-o-y respectively.

Balance sheet and capital expenditure

Operating cash flow amounted to €126m in 3Q24, while capital expenditure reached €59m, directed mainly to maintenance and safety projects at the refineries, alongside maintenance and expansion projects at the Thessaloniki polypropylene plant.

Net debt increased q-o-q to €1.77bn. During 3Q24, the final dividend for the fiscal year 2023 was distributed, amounting to €183m.

Furthermore, in 3Q24 the debt refinancing cycle was successfully concluded, while the Oct’ 24 outstanding notes (€300m) were fully repaid. Over the past 2 years, the Group’s balance sheet and the debt maturity profile have significantly improved, as demonstrated by the extension of the average maturity to five years, along with a re-balanced exposure to floating vs fixed interest rates. Furthermore, the current credit headroom, excluding project finance, exceeds €1.1bn.

Andreas Shiamishis, Group CEO, commented on the results:

“In 3Q24 we achieved very good operational performance in refining, with oil products output reaching a six-year high and sales at an eight-year high, driven by increased availability of our refining units. As expected, 3Q24 financial results were affected by weak benchmark refining margins. Nonetheless, the 9M24 performance remains particularly positive, with the Refining, Supply & Trading business contributing approximately €0.6bn (80%) to the Group Adjusted EBITDA, which amounted to €0.75bn. Notable improvement has also been delivered by the Marketing business in Greece and internationally. At the same time, the RES business’ organic growth is progressing, contributing €50m of annual EBITDA in just 3 years from its inception.

9M24 profitability and the current year’s outlook allow for the distribution of a €0.20 per share interim dividend to shareholders.

The implementation of the Vision 2025 strategic plan continues, with the objective of improving our position in the energy market and our environmental footprint. The results thus far justify the balanced transition to RES and highlight the importance of enhancing operational performance across all core businesses, as well as pursuing international expansion. Furthermore, ongoing initiatives are underway to further improve corporate governance and re-align our business model in the electricity and natural gas markets, with the objective of maximizing the value of the Group.

The development of our human capital, the strengthening of required skills in both core and new activities, and the consolidation of a culture of meritocracy and high performance are the key enablers for achieving our strategic objectives. In the last few years, we have implemented extensive recruitment campaigns, resulting in a staff renewal rate of approximately 40%, with a particular focus on repatriating specialized executives from abroad.”

Key highlights and contribution for each of the main business units in 3Q24 were:

Refining, Supply & Trading

- 3Q24 Refining, Supply & Trading Adjusted EBITDA came in at €95m, lower y-o-y, as the refining margin fell to $10.9/bbl vs $20.5/bbl in 3Q23), despite sustained overperformance.

- Production increased by 6% y-o-y and reached a six-year high, at 4.3m MT, on high refineries availability; likewise, sales volume rose by 8% y-o-y and reached an eight-year high. Exports and sales to bunkering and aviation markets accounted for 72% of total volumes.

Petrochemicals

- 3Q24 Adjusted EBITDA improved by 46% y-o-y to €12m, primarily due to a recovery in polypropylene (PP) margin.

Marketing

- Domestic Marketing recorded improved comparable profitability, primarily due to higher sales across all markets (auto fuels, aviation, bunkering) as well as improved margins. Auto fuels’ market share improved, while the contribution from premium products increased y-o-y for yet another quarter, as well as sales from non-fuel products and services. At the same time, regulatory constraints on the retail gross margin remain in place.

- Performance in International Marketing improved, with increased sales (+3%) and profitability (+14% in Adjusted EBITDA), due to network expansion (327 petrol stations vs 321 in 3Q23), higher margins and contribution from sales of non-fuel products and services.

Renewables

- 3Q24 RES EBITDA amounted to €13m. Installed capacity increased to 384 MW from 356 MW in 3Q23, while power generation stood at 190 GWh, +2% y-o-y).

Associate companies

The contribution of associate companies consolidated using the equity method in the electricity and natural gas sector improved in 3Q24, primarily due to higher profitability from ELPEDISON, and amounted to €4m.