in the aftermath of Russia’s invasion of Ukraine in 2022, but it is nonetheless around double pre-crisis levels. Natural gas supplies have been tightened by the halt of transit of Russian pipeline gas through Ukraine since January 2025 – as well as a return to average winter conditions (after two milder-than-usual winters), driving up withdrawals from gas storage facilities.

In addition, a relatively long period of low wind speeds and limited sunshine in the first half of November – a phenomenon often referred to as Dunkelflaute – required an 80% increase in gas consumption compared with the same period in 2023 to ensure continued electricity supplies. The gas market worldwide also remains tight this year. While global LNG supply growth is expected to accelerate from just 1.5% last year to 5% in 2025, mainly supported by the ramping up of North American LNG facilities, this is partially offset by the halt of Russian piped gas transit via Ukraine.

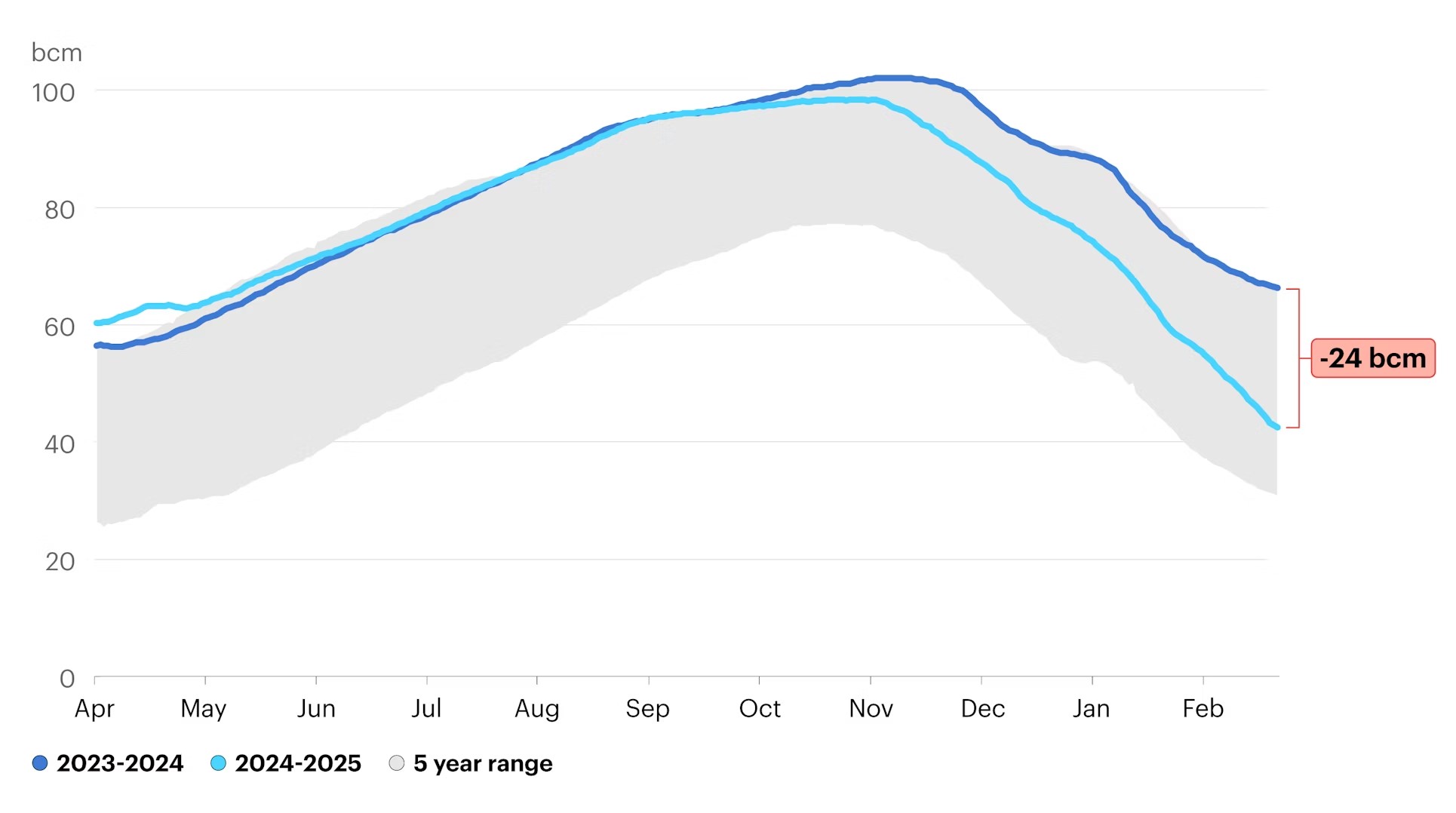

The relatively low amount of gas in storage in the European Union – with levels some 24 billion cubic meters (bcm), or 36%, below where they were this time last year – is putting upward pressure on prices. Meeting EU targets for filling storage before the start of next winter will require much bigger inflows of gas than in the previous two years, increasing Europe’s call on global LNG markets and tightening market fundamentals.

Natural gas storage levels in the European Union

European consumers and governments are now entering their fourth year of high and volatile gas prices. High gas prices have knock-on effects on electricity prices, as well as indirectly on food prices through higher input costs for producers. The economic damage has been visible for both households and businesses; the initial period of the gas price shock was a key contributing factor to inflation and sharp rises in the cost of living, and contributed to higher rates of energy poverty across Europe. Gas prices for industrial consumers in Europe since 2022 have on average been 30% higher than in China and five times as high as in the United States. Several gas- and energy-intensive industries have had to curtail production, and some plants have closed. The elevated gas prices and their broad impacts have complicated efforts by governments to ensure reliable and affordable energy supplies for citizens and companies, and has put the spotlight on the international competitiveness of European industry.

In the EU, the European Commission and member governments have put in place a raft of measures to tame volatility and protect consumers, including the introduction of affordability support measures, gas storage obligations, voluntary targets to cut gas consumption, and a joint gas purchasing mechanism. Although some infrastructure bottlenecks remain, Europe has been able to call on well-meshed gas grids and significant LNG import infrastructure, which enabled it to increase LNG imports rapidly and diversify its gas supplies. Despite Russian piped gas flows to Europe falling by more than 80 bcm (or 50%) in 2022, physical gas supply shortages were avoided.

Since the start of 2022, moreover, around 250 gigawatts of new renewable power capacity have been added across Europe (including the EU, Norway, Switzerland and the United Kingdom), helping to avoid a cumulative total of more than 60 bcm of gas consumption in the electricity sector since then. Although heat pump sales have sharply decelerated from their highs in 2022 and 2023, the 8 million units sold since 2022 have also dampened gas demand during the peak heating season. Europe also made strong improvements in energy efficiency in 2022 and 2023, helping to prevent even greater pressure on supplies and prices, although the rate of efficiency progress ebbed significantly in 2024.

Overall, Europe’s natural gas demand for electricity generation continued to decrease in 2024, falling by 8% and marking the fifth year in a row of annual declines. Alongside these clear signs of structural decline, gas remains essential for the continent’s energy security, including the provision of flexible electricity generation to complement variable renewables such as solar and wind.

At a time of heightened geopolitical and economic uncertainty, European energy systems face a challenging year ahead as the continent emerges from this winter with lower-than-average levels of gas in storage. Global gas markets are unlikely to start to ease significantly until well into 2026 when a huge wave of new LNG supply is set to start hitting international markets. These new LNG projects – most of them in the United States and Qatar – are expected to come online over a period of several years, increasing global LNG export capacity by nearly 50% by 2030, if the projects follow their announced schedules.

But waiting for this new supply is not a viable strategy for European economies facing elevated gas prices today. Between now and then, European governments need to work harder than ever to accelerate energy efficiency improvements, diversify energy supplies and implement other measures to strengthen energy security, including increasing sources of flexibility in electricity systems. In an uncertain geopolitical climate, reminding citizens of the benefits of energy efficiency and gas-saving measures – which improve both energy security and affordability – can go a long way toward demonstrating Europe’s resilience as countries continue to deliver on their goals of building newer, cleaner, more secure and more competitive energy systems. Particular attention needs to be paid to gas supply resilience, with options including the agreement of long-term contracts to provide more stable supplies and strengthening the transatlantic partnership on LNG trade.

*Gergely Molnar, Energy Analyst – Natural Gas

Peter Zeniewski, Senior Energy Analyst

source iea.org