Results were mainly driven by strong international industry backdrop, higher refinery availability and increased exports, improved performance from our international portfolio as well as higher contribution from RES.

Downstream production in FY23 was up by 13% to 14.6m MT and sales volume reached 15.5m MT; exports accounted for 54% of total sales volume, one of the highest on record.

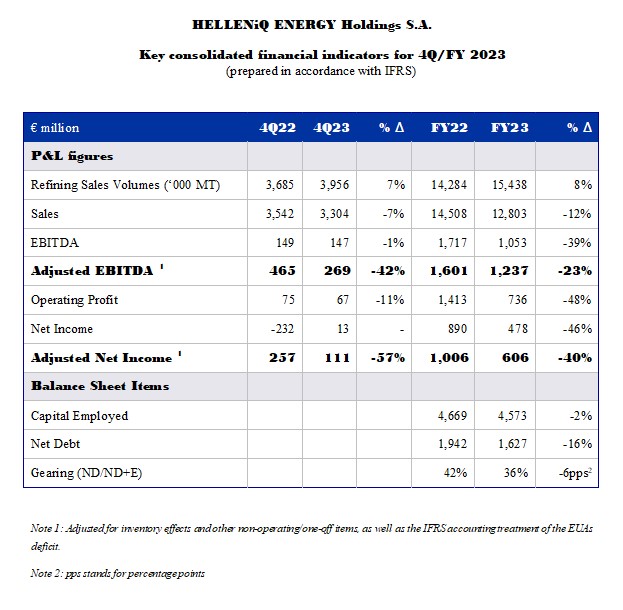

FY23 Reported Net Income amounted to €478m, reflecting a negative impact from crude and products inventory valuation following a decline of international prices since 2022.

Considering the strong performance and outlook, the Board of Directors will propose to the AGM the distribution of a final dividend of €0.60 per share. This will add to the interim dividend of €0.30 per share, which has already been distributed, resulting in a total FY23 dividend of €0.90 per share. Using the 2023 year-end share price, the total dividend represents a higher than 12% dividend yield.

Strategy Implementation - Vision 2025

During 2023, the Group recorded progress in all strategic areas and has implemented significant initiatives that will deliver value upon their completion in the coming years.

The objective in our core business, is to further enhance financial performance and accelerate projects that profitably promote energy transition. In this context, we are progressing projects that improve energy efficiency and increase energy autonomy in the downstream business, aiming for both improved economics, as well better environmental footprint. As part of the energy transition process, we are implementing a Hydrotreated Vegetable Oil (HVO) co-processing unit in Thessaloniki, an investment that will initiate the substitution of a small part of the fossil fuels output. Additionally, investments are being evaluated for the first Greek Sustainable Aviation Fuel (SAF) production unit in Aspropyrgos, the implementation of a CO2 capture project in Elefsina, a project that is highly dependent upon regulatory framework and EU/national strategy, as well as the production of green hydrogen and synthetic fuels in Elefsina and Thessaloniki. These solutions are of great significance, as they support the reduction of the Company's carbon footprint and help transition the transportation fuels sector to a greener future. Finally, the expansion of the polypropylene production plant is already in progress, which, further to economic value increase, it reduces our reliance on fuel sales and further improves environmental impact of our business.

In Fuels Marketing, the continuous expansion of the international network, the promotion of e-mobility and the ongoing improvement of our service stations, which are key to the delivery of our value proposition to the end-consumer, remain a key priority.

In the RES business, HELLENiQ Renewables has significantly accelerated the expansion of its portfolio in 2023, positioning itself as a leading player in both the Greek market and selected international markets. Specifically, through the completion of a series of agreements in Greece, Cyprus and Romania, it had achieved an installed capacity of 356 MW by the end of 2023, along with projects under construction or in advanced stages of development with a total capacity of 0.7 GW. The current pipeline has increased further to 4.3 GW, with growing aspirations for our international footprint as well. The progress achieved to date credibly supports our claim of attaining an operational capacity of over 1 GW by 2025 and more than 2 GW by 2030.

In the E&P business, the acquisition of 3D seismic data in three offshore areas ("Ionian", "Block 2", "Block 10") was completed. Furthermore, the acquisition of 2D seismic data in two offshore areas in Crete has been finalized, with data processing currently under way. In Crete, 3D seismic surveys are ongoing and are expected to contribute to further evaluation and the final decisions for next steps.

The implementation of the digital transformation program is ongoing, with an investment of €50m to date and an annualized benefit of €44m in 2023, which is expected to exceed €50m in 2025.

Normalization of crude oil prices and refining margins in 2023

Despite the recovery of international crude oil prices during 2H23, primarily due to the reduction of OPEC+ output, crude oil prices for FY23 normalized compared to the particularly high average prices of 2022. Specifically, the Brent crude averaged $83/bbl, down by 18% y-o-y. In 4Q23 the average price was $84/bbl, 12% lower y-o-y.

The Euro strengthened against the US dollar by 3% averaging 1.08 in 2023, up from 1.05 in 2022.

Refining margins in 2023 declined from FY22 all-time highs, but remained strong compared to the most recent five-year cycle (2015-2019), prior to the pandemic. They were primarily driven by demand for main products, as well as the sanctions imposed on Russia and the geopolitical tensions in Middle East in 4Q23. Our refineries’ system benchmark margin averaged $9.8/bbl in 2023 compared to $11.8/bbl in 2022, while for 4Q23 it averaged $8.2/bbl vs $13.3/bbl in 4Q22.

Improved demand for motor, aviation and marine fuels

Domestic market demand reached 6.6m MT in 2023, -3% y-o-y, due to a drop in heating oil demand. Excluding heating oil, demand rose by 4%, with gasoline and diesel consumption improving by 3% to 4.91m MT. Aviation and marine fuel demand reached 1.45m MT (+7%) and 2.7m MT (+3%) respectively.

Balance sheet and capital expenditure

Thanks to a strong financial performance in FY23, operating cash flows amounted to €965m, while capital expenditure reached €291m, primarily directed to refinery maintenance and infrastructure upgrading projects, with a smaller portion allocated to Marketing and RES. It is anticipated that total capital expenditure for 2024 will increase, mainly due to the acceleration of RES capacity development.

As a result of significant free cash flow generation and despite the gradual payment of the solidarity contribution (€200m in 2023 out of a total amount of €267m) and the distribution of dividends totaling €229m, Net Debt decreased by €0.3bn to €1.63bn, while Gearing (Net Debt to Capital Employed) fell to 36% compared to 42% in 2022.

Furthermore, in 2023 the refinancing of debt totaling €1.2bn was successfully completed, improving the maturity profile, while available credit lines as at the end of 2023 amounted to €1.1bn.

Andreas Shiamishis, Group CEO, commented on the results:

"The Group concluded 2023 as yet another successful year, with the first phase of the Vision 2025 strategic plan almost completed and having a positive impact in terms of operational performance and profitability. Following the unprecedented and exceptional highs of last year, 2023 results, albeit lower than last year, are still very good and the qualitative analysis supports an optimism about the next few years.

Initially, a substantial portion of the 2023 profitability was driven by improvements in the Company's operations and the execution of the strategic transformation program and operational excellence. These are factors that are more controllable and predictable than a volatile international commodity environment which, nevertheless, can have a material impact on the results of the Company. Our efforts include the strengthening of the International Marketing business, expansion into new markets for either fuels products or RES projects, and a substantial renewal and development of our human capital, supporting an ongoing cultural shift across the organization.

An even more important point to note is the gradual departure from a more extreme, if not condemning, approach towards the energy sector, with a shift towards realism. This shift acknowledges that fossil fuels are part of the solution and should contribute to the energy transition in a more environmentally friendly manner. Highlighting this message is the official conclusion, for the first time at the recent COP28, that extreme and unfeasible solutions have a detrimental impact on the environment. They hinder medium-term investments which would otherwise improve existing energy sector performance in the medium term and pave the road towards the future state, while at the same time compromising energy cost and security, particularly in Europe.

Referring to our financial performance, 2023 strong profitability, with Adjusted EBITDA and Adj. Net Income of €1.24bn and €0.6bn respectively, has further solidified the Group's position and based on that, the Board of Directors will propose to the AGM a final dividend of €0.60 per share, resulting in a total dividend of €0.90 per share.

Moreover, alongside the positive financial results, notable progress has been made in ESG matters, including advancements in ESG Key Performance Indicators (KPIs), such as a reduction of over 7% in the CO2 emission index (per activity level), as well as an improvement in ESG ratings with increased participation and contribution to society's needs.

In conclusion, I would like to thank our colleagues, who actively participated in this effort, as well as the shareholders for their trust in the Company throughout the years. I would also like to extend my appreciation to the new shareholders who appreciated in the Group's prospects and participated in the recent placement of 11% of the Company's shares, in an effort undertaken by our main shareholders to expand the investor base."

Key highlights and contribution for each of the main business units in 4Q/FY 23 were:

Refining, Supply & Trading

Refining, Supply & Trading Adjusted EBITDA came in at €236m in 4Q23 and at €1,043m in FY23, supported by high international refining margins, the system’s overperformance and increased sales volume (+8% in FY23) on the back of increased refineries’ availability. Exports accounted for 54% of total sales, up from 49% in FY22.

Production came in at 16.2m MT in FY23, +14% y-o-y, while contribution of high-value-added products in the product mix surpassed 80%.

Petrochemicals

FY23 Adjusted EBITDA came in at €43m, lower y-o-y, on weak PP margins.

Marketing

Despite a 2% decline in Domestic Marketing’s total sales volume in 2023, automotive sales volume increased by 4%, with improved market shares and higher contribution from premium products. Aviation and bunkering sales volume rose by 2% and 1% respectively. Excluding the impact from inventory valuation and the pricing timing on aviation fuels, profitability was broadly stable y-o-y, with regulatory constraints on retail gross margin remaining in place.

International Marketing recorded higher sales volume in 4Q23 and FY23, with profitability at slightly lower levels y-o-y on lower margins at some markets.

Renewables

Higher RES operating capacity (356 ΜW) led to 8% increase in power generation in 4Q23 and by 39% in FY23, with Adjusted EBITDA coming in at €8m and €42m (+44%) respectively.

Associate companies

In FY23 the contribution from associate companies, which are consolidated using the equity method, came in at €18m, lower y-o-y. Specifically, a) Elpedison's profitability was adversely affected by the lower availability of the Thisvi power plant, while b) DEPA's contribution was primarily impacted by lower domestic market demand, reduced margins and increased costs associated with securing capacity in the gas network.